Double-Digit Monthly Gains in Median Home Prices Likely a Thing of the Past

June Sales Volume Lowest Since 2008

California single-family home and condominium sales gained 0.6 percent in June 2014 but were down 12.6 percent from June 2013. Year-to-date sales for the first six months of the year are the lowest since 2008. For the month, non-distressed property sales increased 2.8 percent while sales of distressed properties fell 9.1 percent.

“June marks the sixth consecutive month that sales have been lower on a year-over-year basis,” said Madeline Schnapp, Director of Economic Research for PropertyRadar. “The lack of distressed property inventory and rapid increase in median prices has definitely taken a toll on demand.”

The June 2014 median price of a California home reached its highest level since December 2007, up 5,000 dollars, or 1.3 percent, to 390,000 dollars from 385,000 dollars in May. On a year-ago basis, median home prices gained 10.0 percent. Driving the month-over-month price increase in June was the 2.8 percent increase in the sales volume of higher-priced non-distressed properties, which accounted for nearly 83 percent of total sales. The median price of non-distressed homes was up only 0.8 percent over last year. The deceleration in price increases is even more apparent at the county level. In March, double-digit price increases occurred in 16 of the 26 largest California counties but by June that number had fallen to eight.

“The nearly uninterrupted double-digit monthly increases in median home prices from August 2012 through March 2014 has slowed considerably,” said Schnapp. “That’s good news for buyers who were finding themselves rapidly priced out of the market.”

In other California housing news:

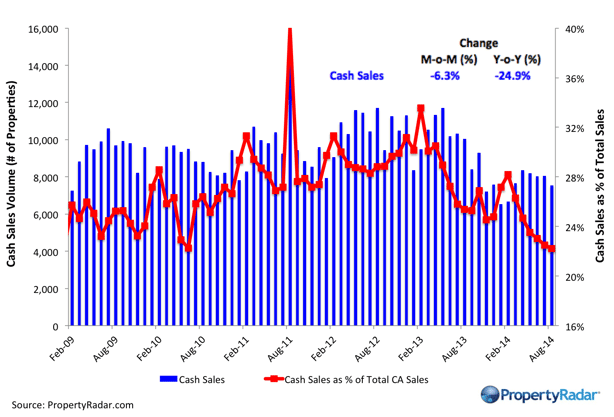

- Cash sales remained elevated in June, accounting for 22.2 percent of total sales. Despite the historically high levels of cash sales, cash sales have been steadily declining, falling 31.6 percent, since reaching an interim peak in May 2013.

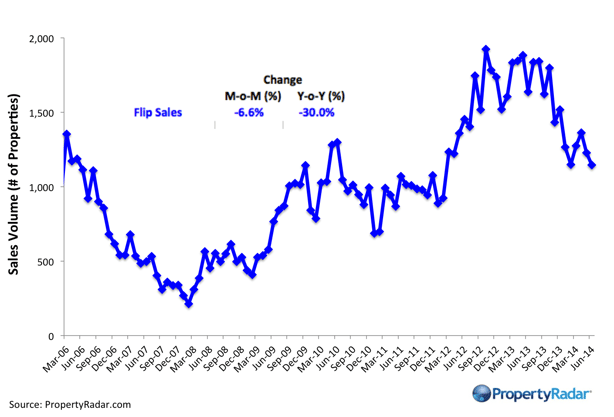

- Flip sales fell 6.6 percent for the month and were down 30.0 percent for the year and are down 40.4 percent from the October 2012 peak.

- Negative equity remains elevated in California and continues to impart negative headwinds to the real estate market. In June, nearly 1.1 million California homeowners, or 12.9 percent remain underwater.

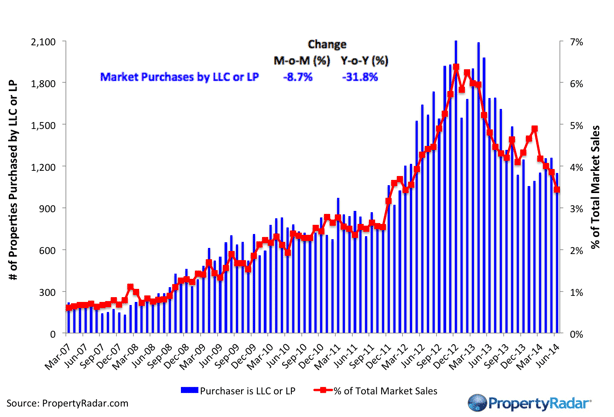

- Institutional Investor LLC and LP purchases fell 8.7 percent for the month and are down 31.8 percent from June 2013. Institutional investor demand continues to wane in the face of higher prices and lower return on investments. Institutional Purchases have posted consistent monthly declines and are down 48.0 percent from their December 2012 peak.

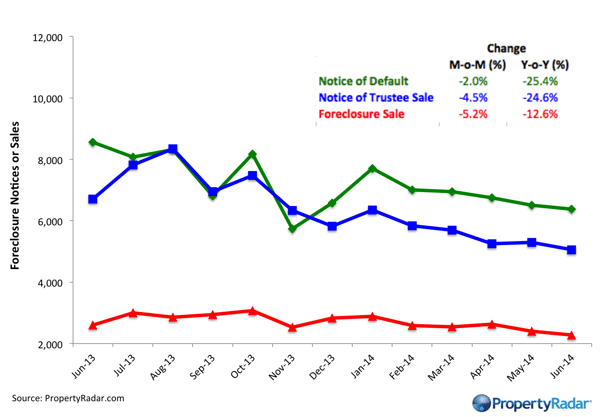

- Foreclosure starts, or Notices of Default (NODs), fell 2.0 percent between May and June, extending a longer-term downward trend. Foreclosure sales fell 5.2 percent for the month and are down 12.6 percent for the year. The June decline decelerated compared to May.

“Affordability and tight credit have slowed or stopped price increases despite lack of inventory,” said Schnapp. “Going forward, we expect low sales volumes and flat prices until increased supply or looser credit forces prices lower.”

Home Sales

Home Sales - Single-family residence and condominium sales by month from 2007 to current divided into distressed and non-distressed sales. Distressed sales are the sum of short sales, where the home is sold for less than the amount owed, and REO sales, where banks resell homes that they took ownership of after foreclosure. All other sales are considered non-distressed.

Year-over-Year Home Sales

Year-over-Year Home Sales - Single-family residences and condominiums sold during the same month for the current year and prior years divided into distressed and non-distressed sales.

Median Sales Prices vs. Sales Volume

Median Sales Price vs. Sales Volume - Median sales price (left axis) of a California single family home versus sales volume (right axis), by month from 2005 to current. Median sales prices are divided into three categories: All single-family homes (blue line), distressed properties (red line), and non-distressed properties (green line). Monthly sales volume (right axis) are illustrated as gray and lavender bars. The gray bars are distressed sales and the lavender bars are non-distressed sales.

California Homeowner Equity

California Home Owner Equity - A model estimate of California homeowners segregated into various categories of levels of homeowner equity for a given month. Homeowner numbers represent a percentage of total California homeowners.

Cash Sales

Cash Sales - The blue bars (right axis) illustrate cash sales of single-family residences and condominiums by month. The red line (left axis) illustrates cash sales as a percentage of total sales by month.

Flipping

Flipping – The number of single-family residences and condominiums resold within six months.

Market Purchases by LLCs and LPs

Market Purchases by LLCs and LPs - The blue bars (right axis) illustrate market purchases of single family residences and condominiums by LLCs and LPs from 2007 to current. The red line graph (left axis) illustrates LLC and LP purchases as a percentage of total sales by month.

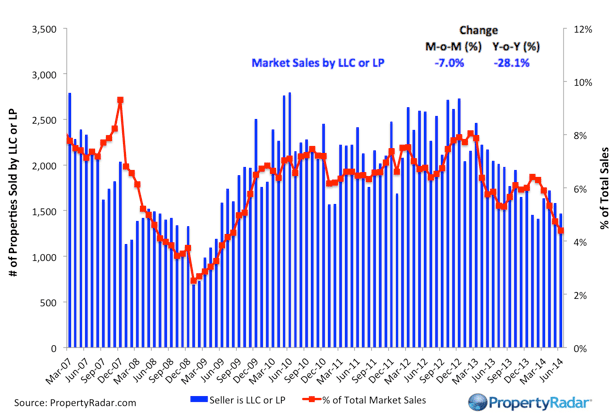

Market Sales by LLCs and LPs

Market Sales by LLCs and LPs - The blue bars (right axis) illustrate market sales by LLCs and LPs of single-family residences and condominiums by month. The red line graph (left axis) illustrates sales as a percentage of total sales by month.

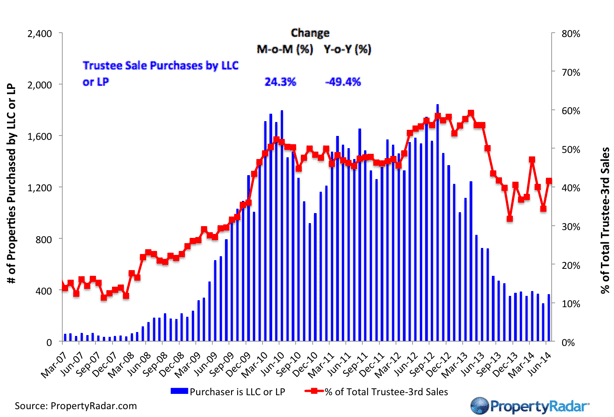

Trustee Sale Purchases by LLCs and LPs

Trustee Sale Purchases by LLCs and LPs - The blue bars (right axis) illustrate trustee sale purchases (foreclosure sales) of single-family residences and condominiums by LLCs and LPs from 2007 to current. The red line graph (left axis) illustrates purchases as a percentage of total trustee sales by month.

Foreclosure Notices and Sales

Foreclosure Notices and Sales - Properties that have received foreclosure notices — Notice of Default (green) or Notice of Trustee Sale (blue) — or have been sold at a foreclosure auction (red) by month.

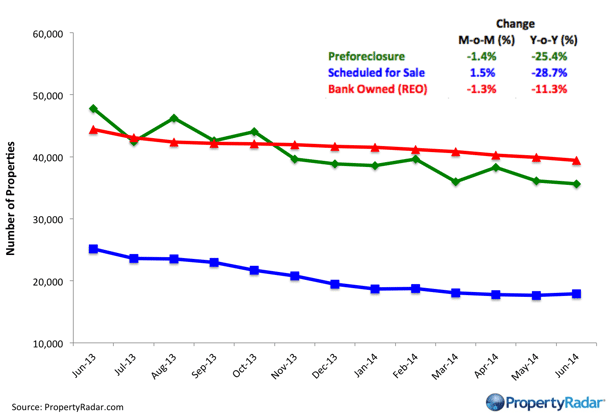

Foreclosure Inventories

Foreclosure Inventory - Preforeclosure inventory estimates the number of properties that have had a Notice of Default filed against them but have not been Scheduled for Sale, by month. Scheduled for Sale inventory represents properties that have had a Notice of Trustee Sale filed but have not yet been sold or had the sale cancelled, by month. Bank-Owned (REO) inventory means properties sold Back to the Bank at the trustee sale and the bank has not resold to another party, by month.

Real Property Report Methodology

California real estate data presented by PropertyRadar, including analysis, charts, and graphs, is based upon public county records and daily trustee sale (foreclosure auction) results. Items are reported as of the date the event occurred or was recorded with the California county. If a county has not reported complete data by the publication date, we may estimate the missing data, though only if the missing data is believed to be 10 percent or less of all reported data.