Normal Seasonal Forces Slow California Real Estate Sales

November Sales Tumble 17.6 Percent Month-over-Month

Median Prices Flat

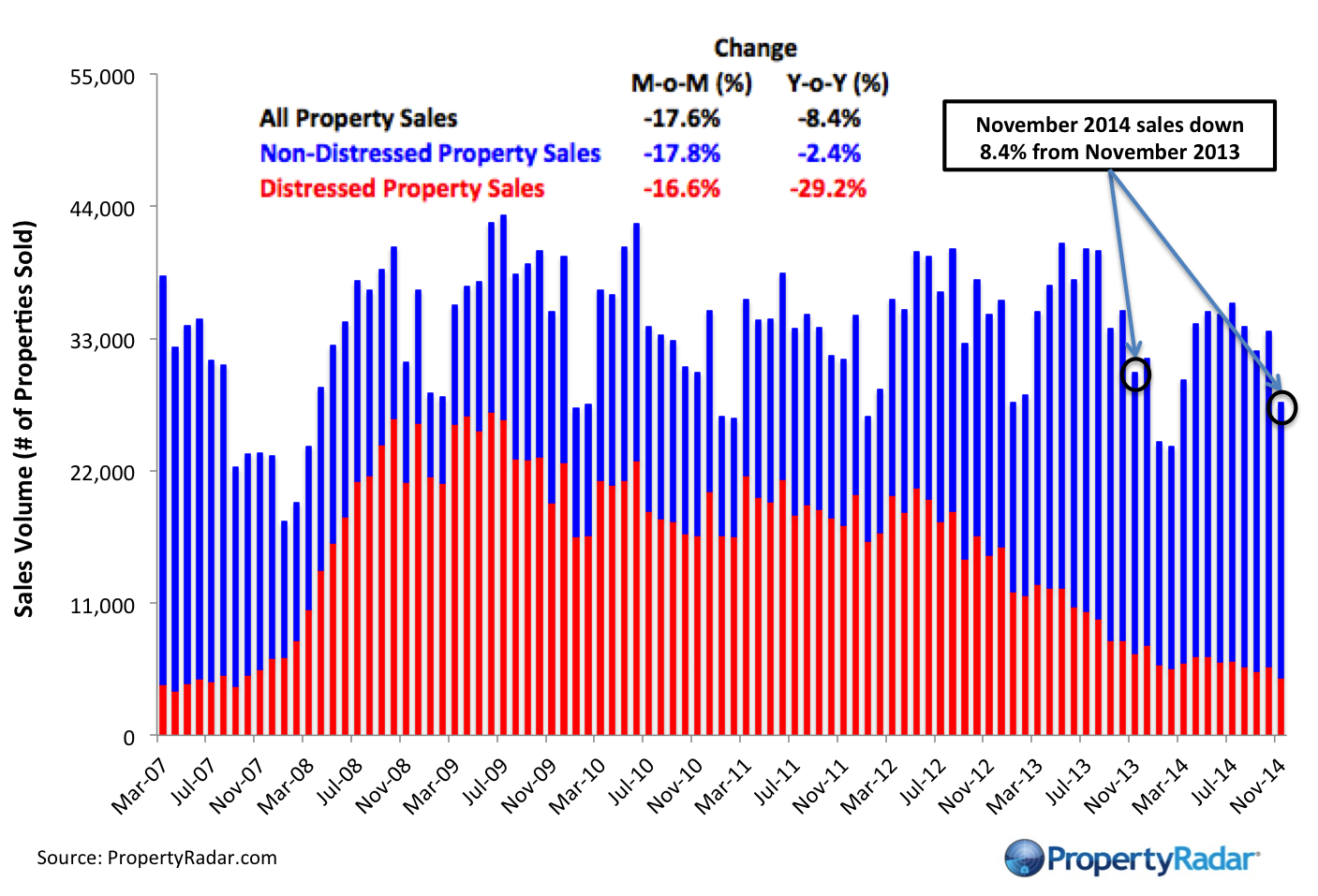

As is typical during the late fall and winter season, real estate sales declined in November. California single-family home and condominium sales fell 17.6 percent to 27,649 units from 33,561 in October. Year-over-year, sales were down 8.4 percent from 30,184 sales in November 2013. On a regional basis, for the month, sales declined 31.7 percent in the Bay Area, 21.3 percent in Southern California, and 24.8 percent in the Central Valley.

“The California real estate market has entered its annual hibernation period characterized by much lower sales,” said Schnapp, Director of Economic Research for PropertyRadar. “Median prices will likely trend sideways until next spring when the selling season begins anew.”

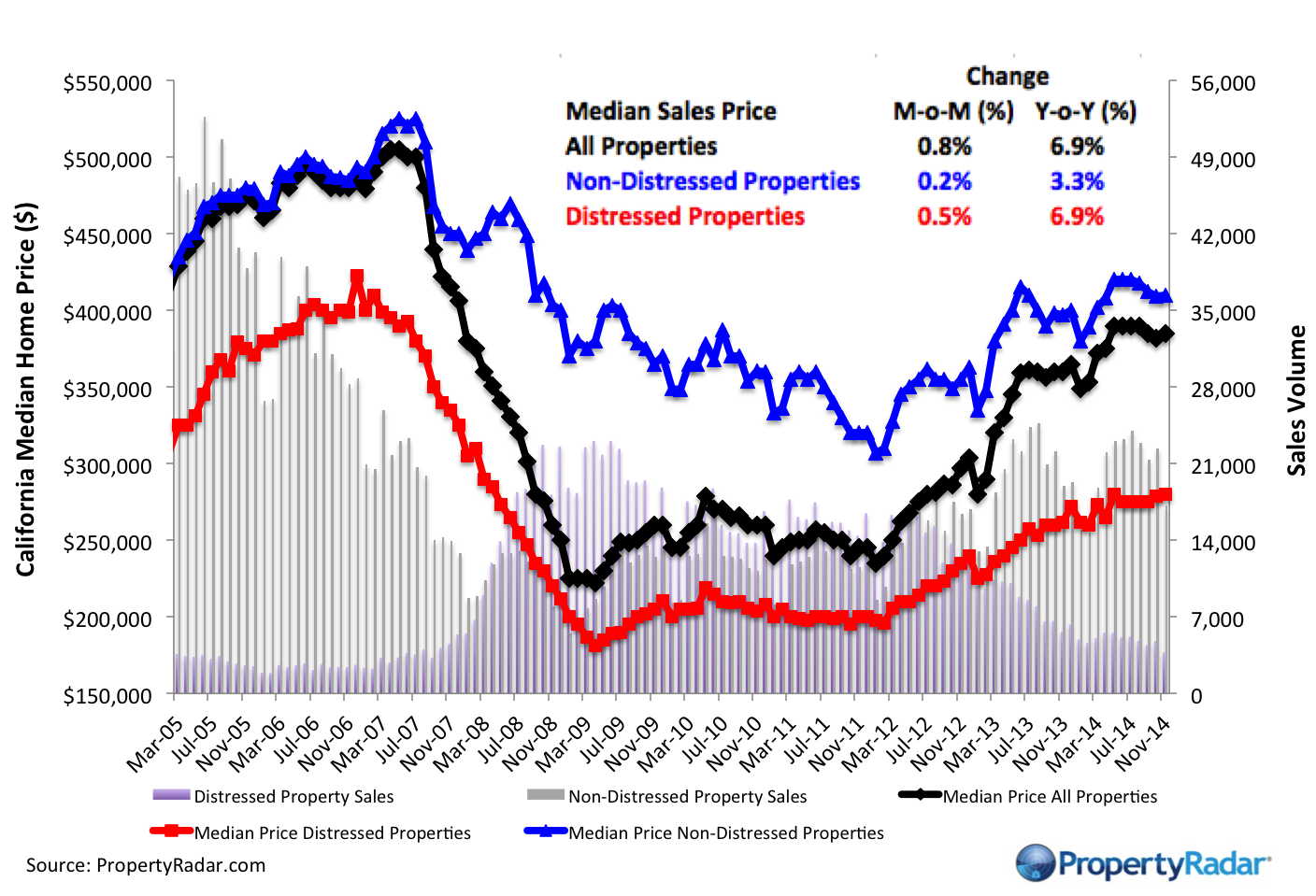

The median price of a California home in November was 385,000 dollars, up 3,000 dollars, or 0.8 percent from 382,000 dollars in October. Median prices have been more or less unchanged since May 2014. On a year-ago basis, median home prices gained 6.9 percent.

“As has been the case all year, high prices hampered home sales this past month,” said Schnapp. “The new lower 3 percent down payment option recently announced by Fannie Mae and Freddie Mac should help boost sales next year.”

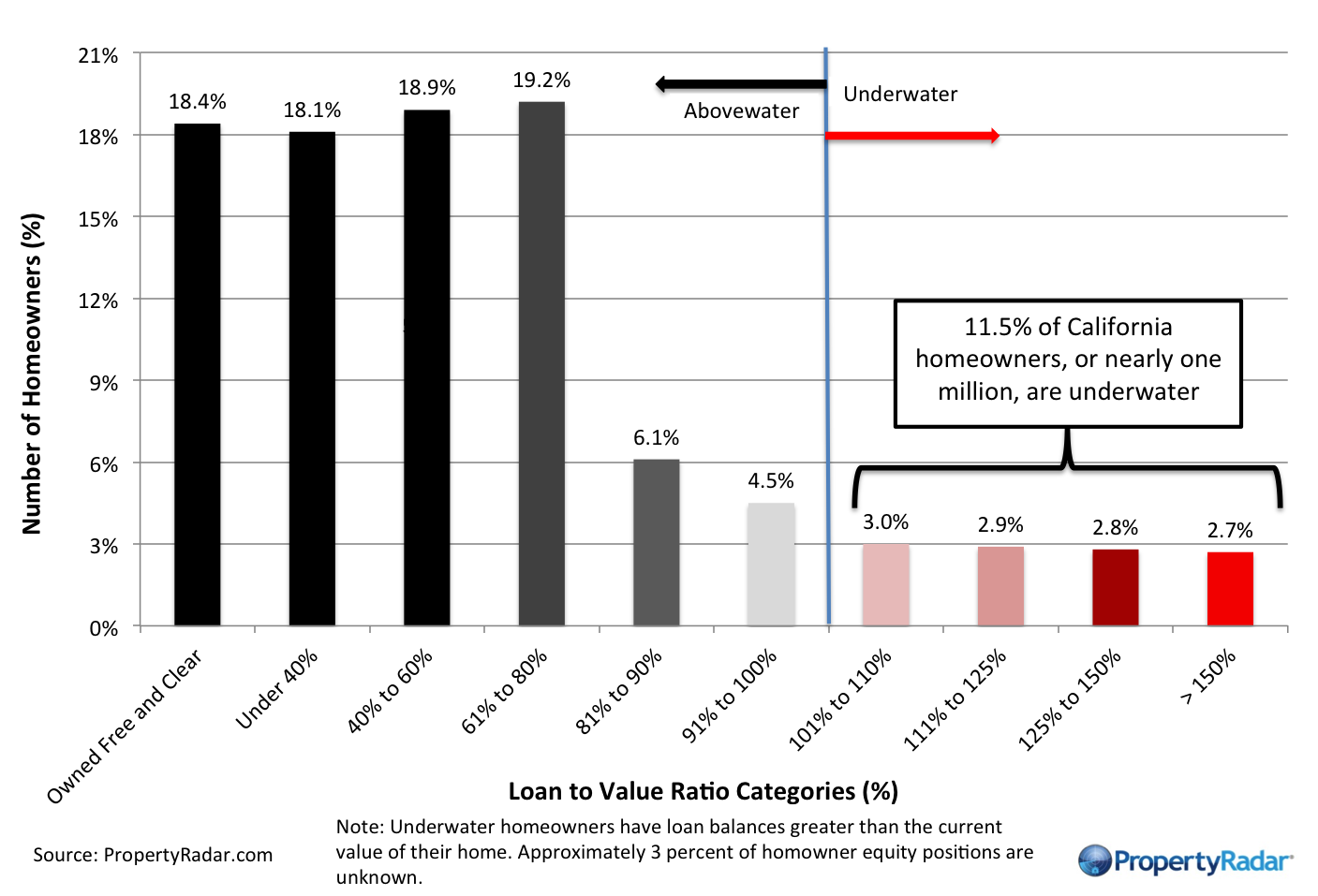

The number of homeowners in a negative equity position fell below one million homeowners in November. At the end of November, 998,000 California homeowners, or 11.5 percent were underwater.

“The California real estate market hit a milestone this past month when the number of homeowners that owe more than their home is worth fell below the one million mark,” said Schnapp. “That’s good news for the California market since those homeowners can now buy or sell and become active participants in the market.”

In other California housing news:

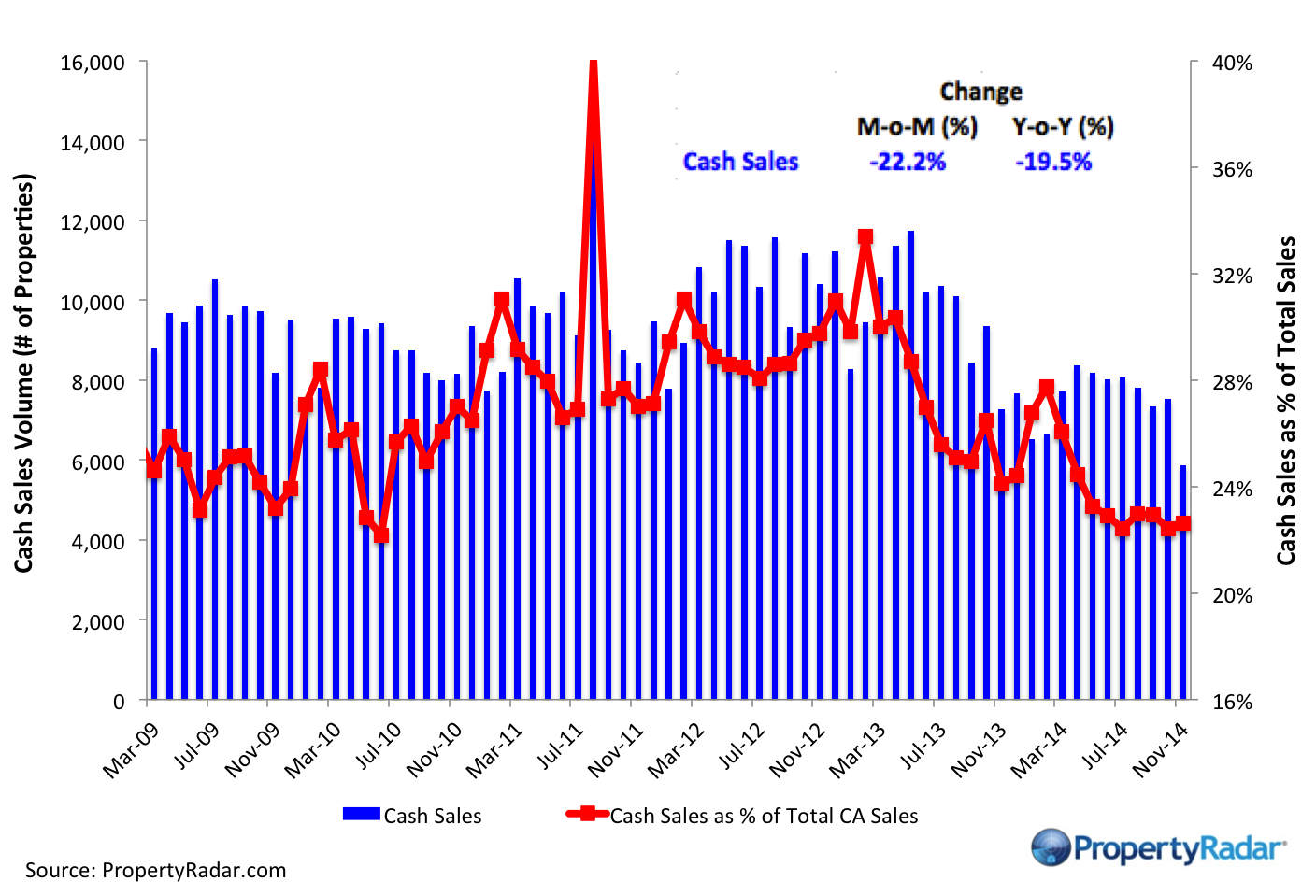

- As is typical for this time of year, cash sales retreated for the month. November cash sales fell 22.2 percent to 5,857, down from 7,524 in October and were 22.6 percent of total sales. Cash sales have been steadily declining since reaching a peak of 40.0 percent of total sales, or 14,028, in August 2011. Since then, cash sales have fallen 58 percent. Within the 26 largest counties of California, cash sales as a percentage of total sales were highest in Merced, Santa Cruz, and Sonoma counties at 28.8, 28.9, and 27.0 percent, respectively.

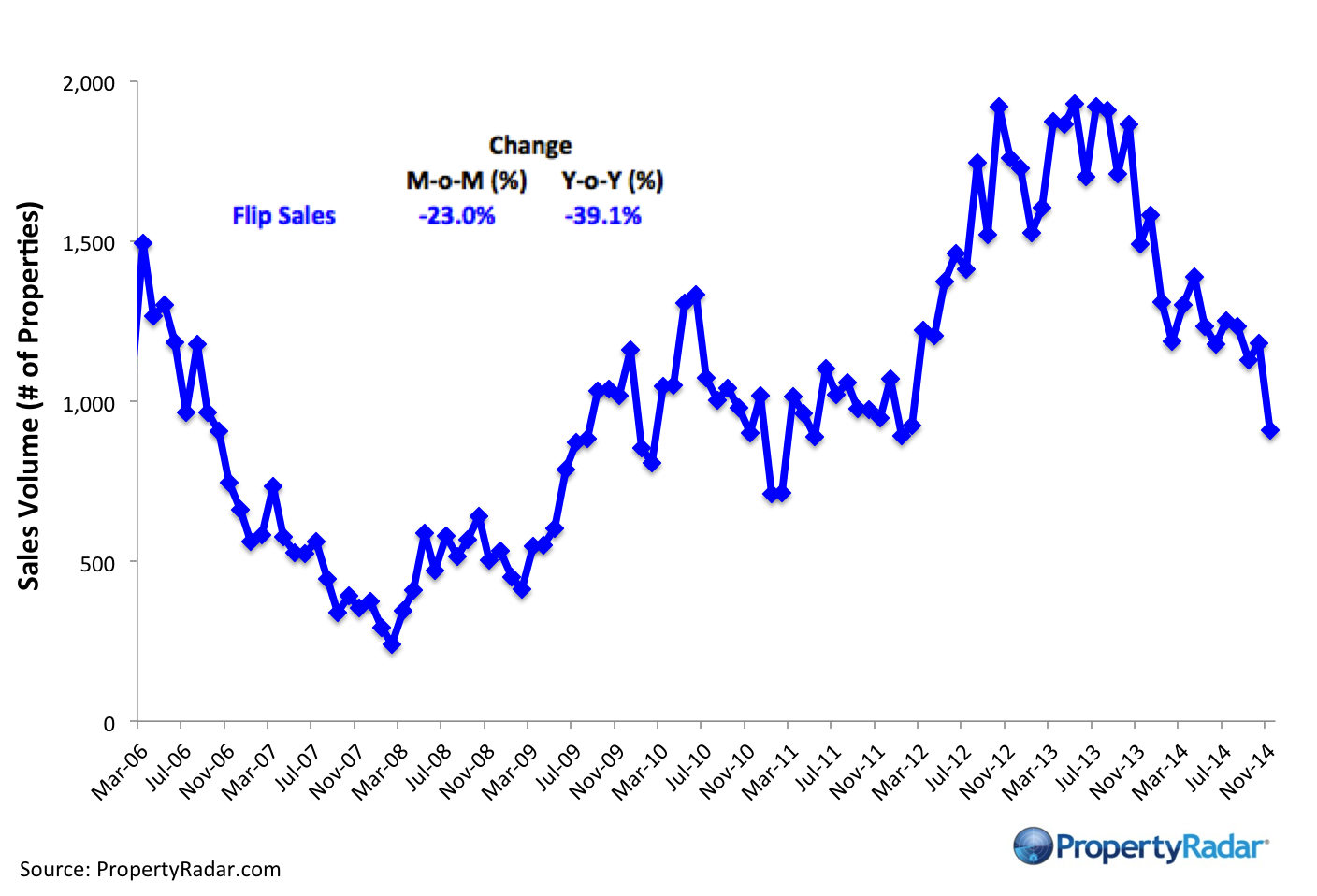

- Flip sales fell 23.0 percent for the month and are down 39.1 percent for the year. Flip sales are defined as properties that have been resold within six months. Flip sales comprised 3.6 percent of total sales in November, up 0.1 percent from October. Flip sales peaked in May 2013 at 5.1 percent of total sales and have declined 52.9 percent since then. Within the 26 largest counties in California, Kern, San Diego, and Tulare had the highest percentage of flips at 5.3, 4.8, and 5.1 percent, respectively.

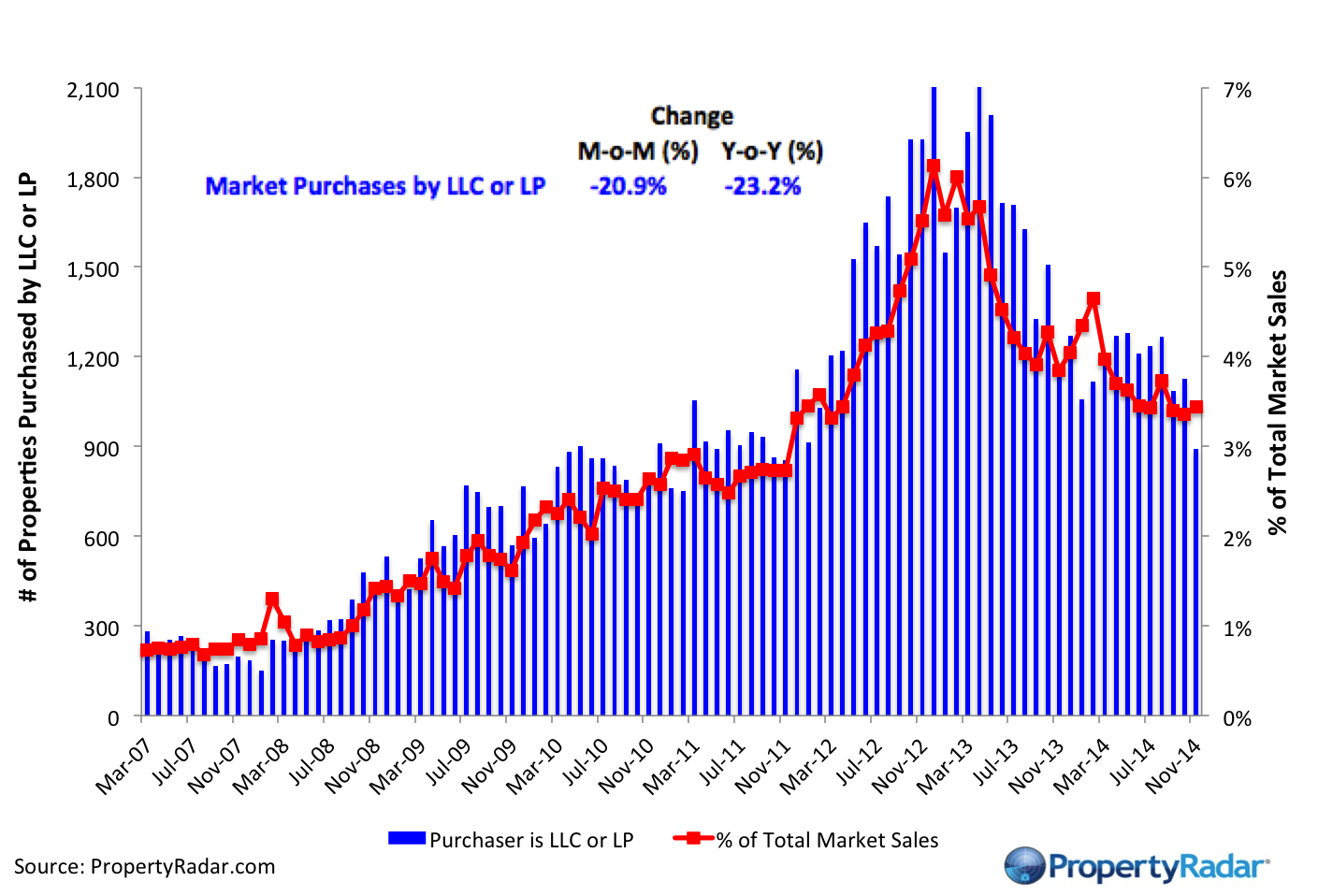

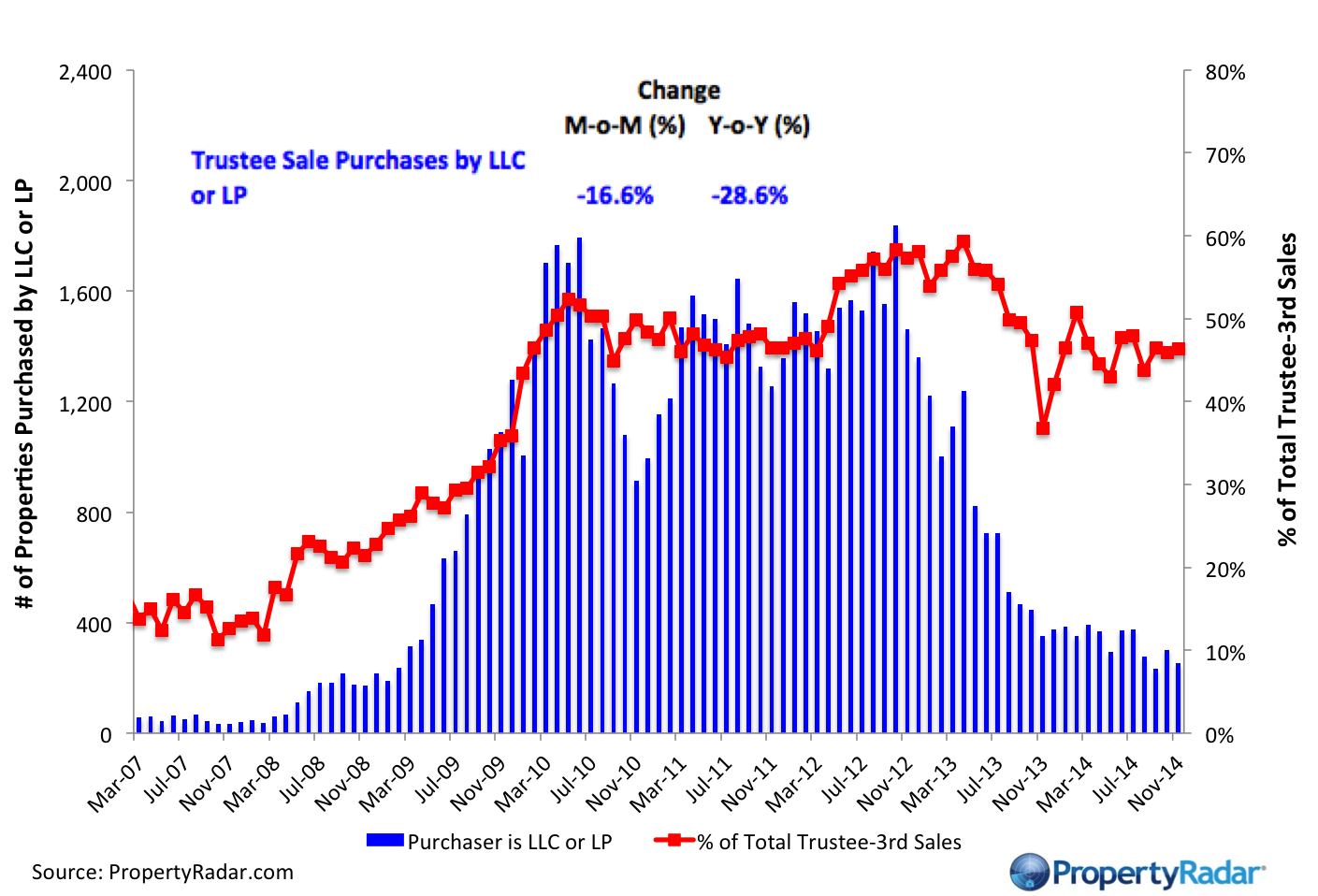

- Institutional Investor LLC and LP purchases fell 20.9 percent for the month and are down 23.2 percent from November 2013. Outsized monthly declines are normal for this time of year and will likely rebound somewhat in Q1-2015. Over the longer term, however, as the supply of distressed properties dwindle and prices rise, institutional investor demand has retreated due to the lower return on investment. In general, Institutional Purchases have posted consistent monthly declines since peaking in December 2012 and are down 59.8 percent since then. Trustee sale purchases by LLC and LPs are down 85.5 percent from their October 2012 peak.

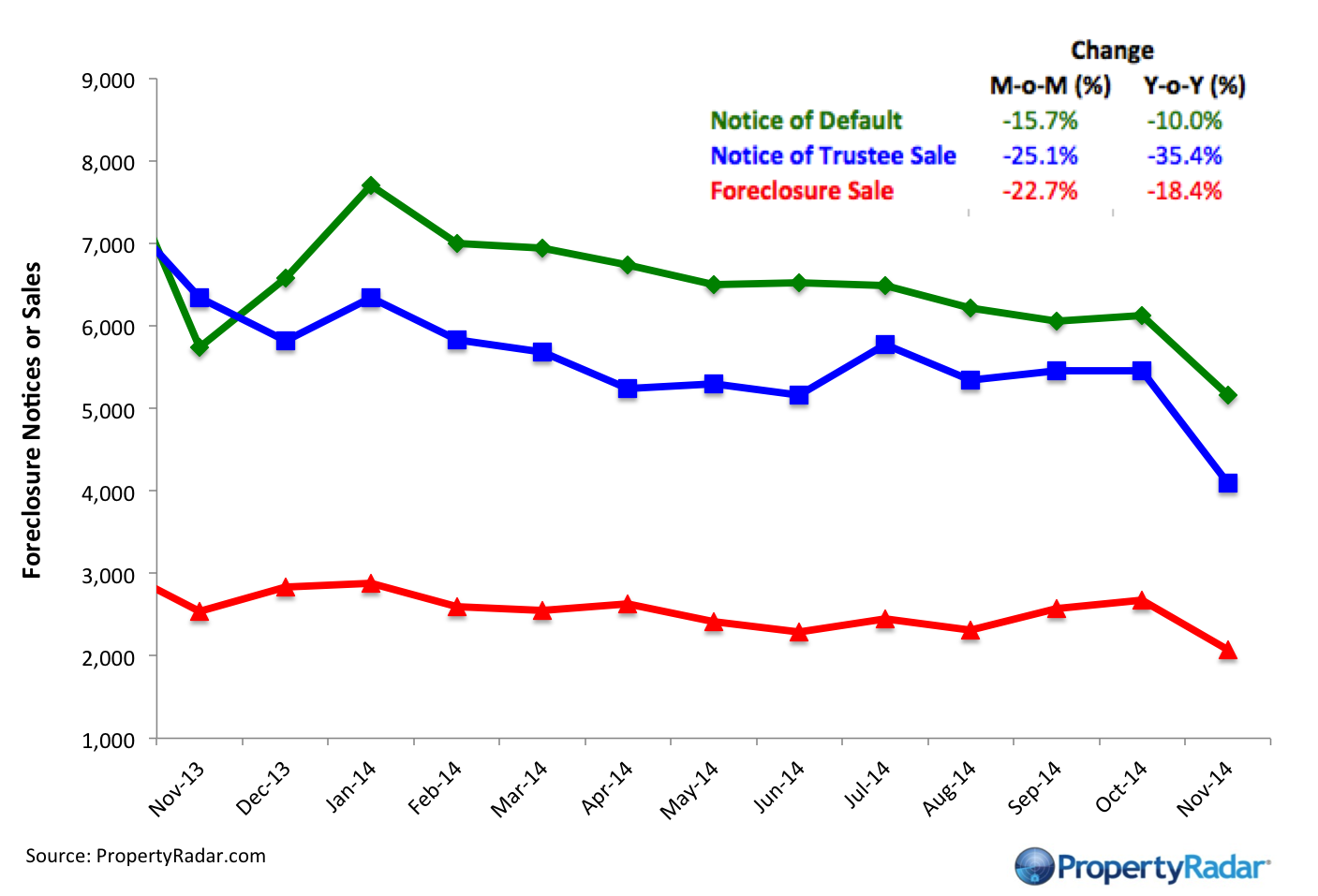

- Foreclosure starts, Notices of Default (NODs), fell 15.7 percent between October and November and are down 10.0 percent from November 2013. The larger-than-normal monthly decline is typical during the holiday season. Foreclosure Sales fell 22.7 percent for the month and are down 18.4 percent for the year.

Home Sales

Home Sales - Single-family residence and condominium sales by month from 2007 to current divided into distressed and non-distressed sales. Distressed sales are the sum of short sales, where the home is sold for less than the amount owed, and REO sales, where banks resell homes that they took ownership of after foreclosure. All other sales are considered non-distressed.

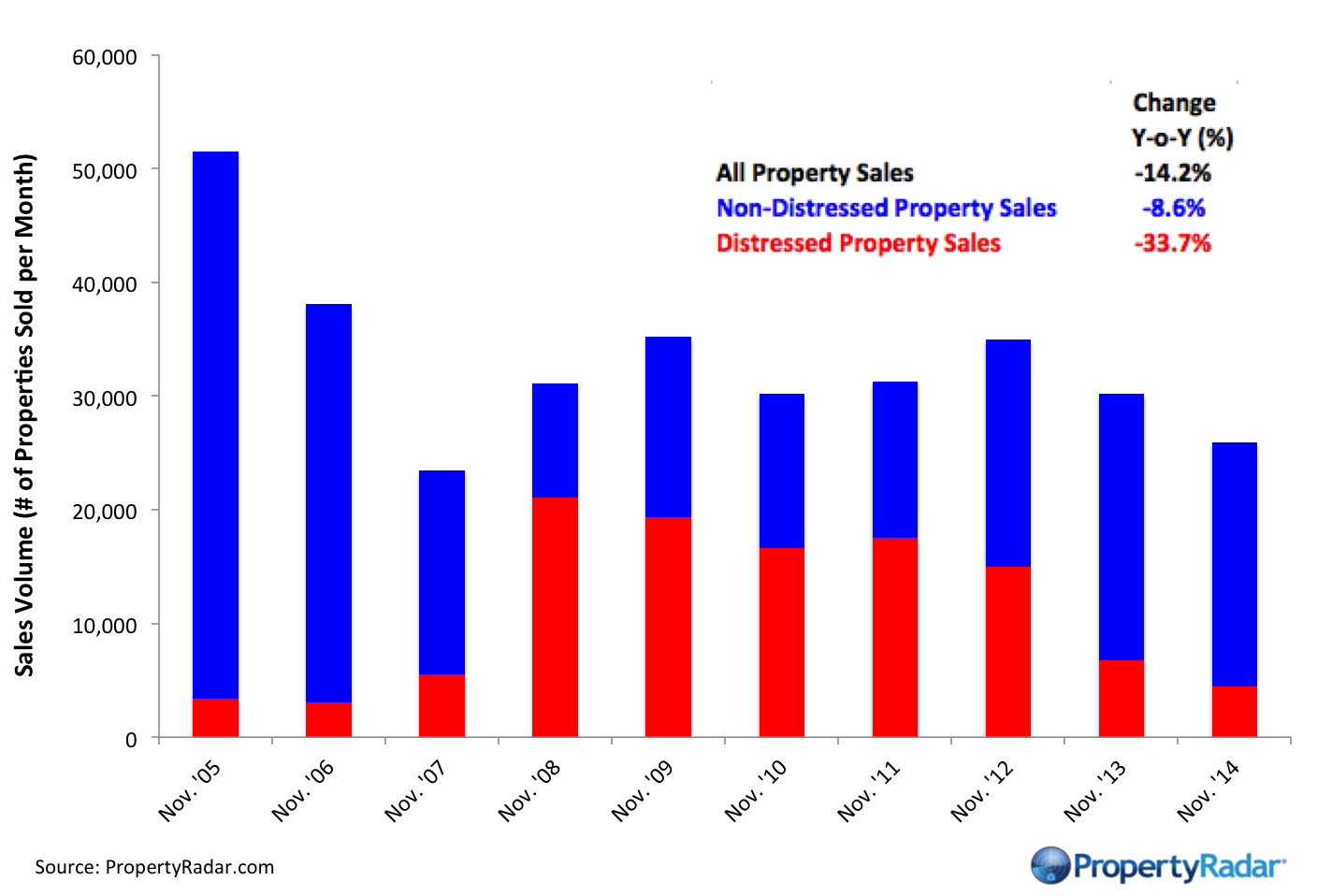

Year-over-Year Home Sales

Year-over-Year Home Sales - Single-family residences and condominiums sold during the same month for the current year and prior years divided into distressed and non-distressed sales.

Median Sales Prices vs. Sales Volume

Median Sales Price vs. Sales Volume - Median sales price (left axis) of a California single-family home versus sales volume (right axis), by month from 2005 to current. Median sales prices are divided into three categories: All single-family homes (blue line), distressed properties (red line), and non-distressed properties (green line). Monthly sales volume (right axis) are illustrated as gray and lavender bars. The gray bars are distressed sales and the lavender bars are non-distressed sales.

California Homeowner Equity

California Home Owner Equity - A model estimate of California homeowners segregated into various categories of levels of homeowner equity for a given month. Homeowner numbers represent a percentage of total California homeowners.

Cash Sales

Cash Sales - The blue bars (right axis) illustrate cash sales of single-family residences and condominiums by month. The red line (left axis) illustrates cash sales as a percentage of total sales by month.

Flipping

Flipping – The number of single-family residences and condominiums resold within six months.

Market Purchases by LLCs and LPs

Market Purchases by LLCs and LPs - The blue bars (right axis) illustrate market purchases of single-family residences and condominiums by LLCs and LPs from 2007 to current. The red line graph (left axis) illustrates LLC and LP purchases as a percentage of total sales by month.

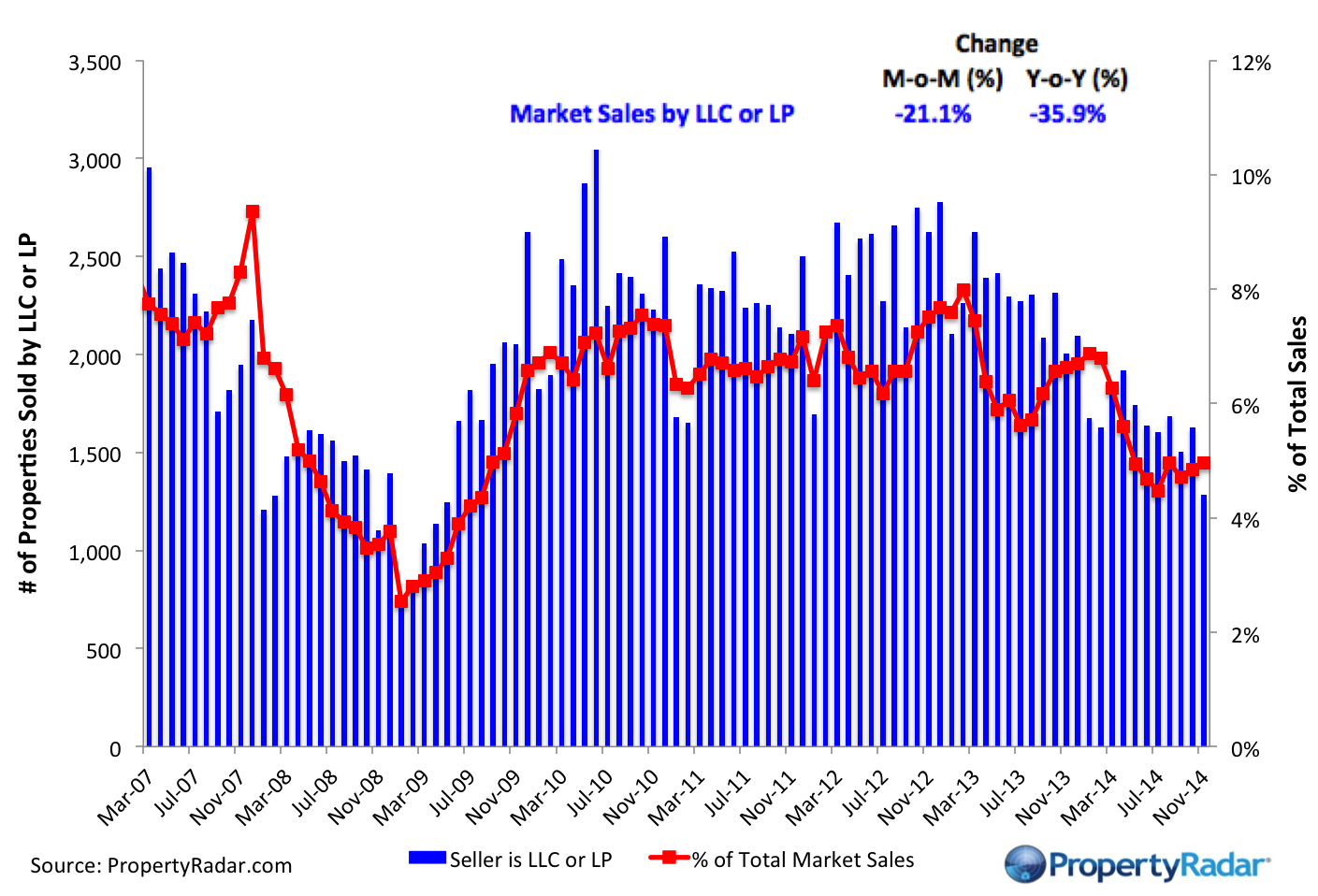

Market Sales by LLCs and LPs

Trustee Sale Purchases by LLCs and LPs

Trustee Sale Purchases by LLCs and LPs - The blue bars (right axis) illustrate trustee sale purchases (foreclosure sales) of single-family residences and condominiums by LLCs and LPs from 2007 to current. The red line graph (left axis) illustrates purchases as a percentage of total trustee sales by month.

Foreclosure Notices and Sales

Foreclosure Notices and Sales - Properties that have received foreclosure notices — Notice of Default (green) or Notice of Trustee Sale (blue) — or have been sold at a foreclosure auction (red) by month.

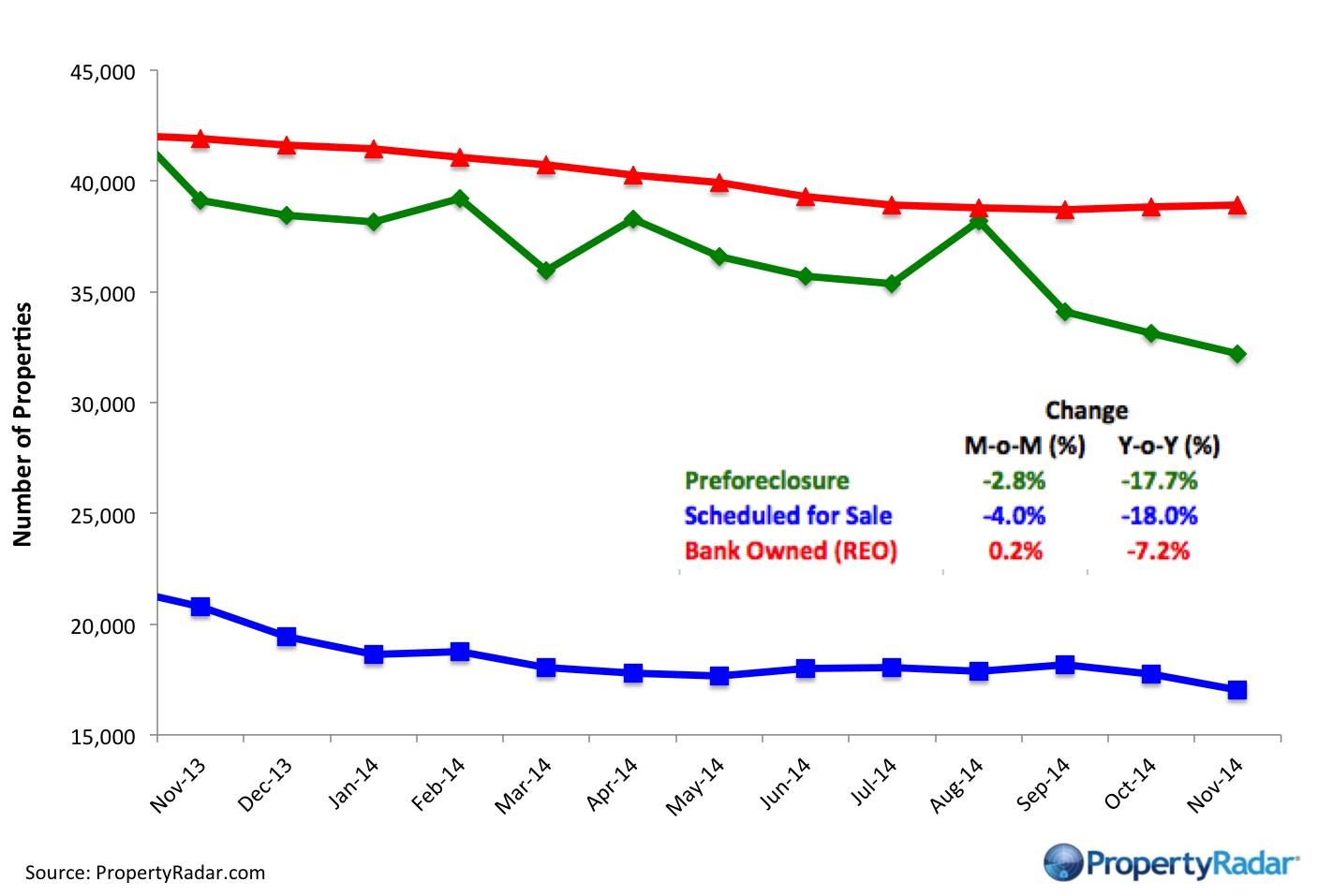

Foreclosure Inventories

Foreclosure Inventory - Preforeclosure inventory estimates the number of properties that have had a Notice of Default filed against them but have not been Scheduled for Sale, by month. Scheduled for Sale inventory represents properties that have had a Notice of Trustee Sale filed but have not yet been sold or had the sale cancelled, by month. Bank-Owned (REO) inventory means properties sold Back to the Bank at the trustee sale and the bank has not resold to another party, by month.

Real Property Report Methodology

California real estate data presented by PropertyRadar, including analysis, charts, and graphs, is based upon public county records and daily trustee sale (foreclosure auction) results. Items are reported as of the date the event occurred or was recorded with the California county. If a county has not reported complete data by the publication date, we may estimate the missing data, though only if the missing data is believed to be 10 percent or less of all reported data.