Record equity in 2022 will make for some exciting opportunities for data driven professionals. Are you ready to strike while the iron’s hot?!

Generating mortgage leads can feel like an unbreakable ebb and flow cycle. But if you’re a data driven mortgage pro who knows where to look, you can skip the ebbs and keep your pipeline full with a consistent flow of mortgage leads no matter the market conditions. And if you’re not a data driven pro yet – you will be after reading this post.

Here’s the deal. Mortgage professionals have had two of the most profitable years on record. Low-interest rates combined with record-breaking home prices meant big business for purchase-money and refinance loans.

Most industry associations are predicting that home price appreciation will slow in 2022. Recent unemployment and inflation data have many predicting that the Fed will increase interest rates as soon as Spring 2022. Rising mortgage rates cause concern for fear it could end the purchase money and refinance boom.

|

|

However, data-driven mortgage professionals know that despite these industry headwinds, mortgage professionals will thrive in 2022 by focusing on strategies that take advantage of this unusual market cycle and the massive equity gains that have occurred in record time.

Mortgage

Record Equity Gains

There was little way to know how the pandemic would shape consumer behavior in housing. With businesses creating work-from-home and hybrid work models, consumers could reimagine and reprioritize life. Suddenly, the home became where you live, work, play, and educate. Consumers had the flexibility to move closer to family, relocate to places with more space, and find properties that better fit their needs and budget.

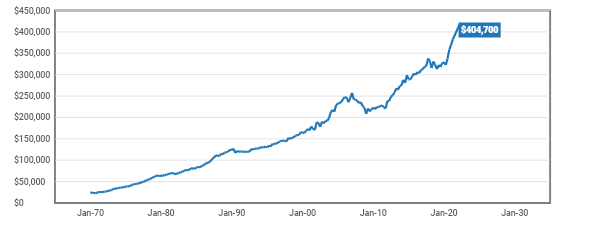

Strong demand combined with low inventory was a recipe for record-breaking price appreciation and massive equity gains. The US Census shows the median sales price grew 19.9% from Q3-2020 to Q3-2021, now $404,700. The only comparable year is 1973, when home prices increased 20.1% in that same year-over-year timeframe. That loan you originated only one year ago is now likely sitting on close to 20% equity!

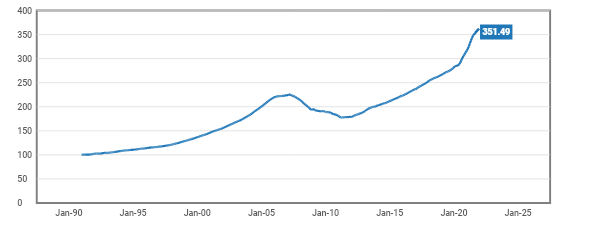

In November, The Federal Housing Finance Authority (FHFA) released the 2022 conventional loan limits for Fannie Mae and Freddie Mac. FHFA uses the Housing Price Index (HPI) to calculate new limits. From Q3-2020 to Q3-2021, the index rose 18%. The new conforming limit for single-family homes also increased 18% from $548,250 in 2021 to $647,200, a nearly $100,000 increase. High-cost areas increased from $822,375 in 2021 to $970,800. For reference, in 2016 those limits were $424,100 and $721,050, respectively.

With these new loan limits, qualifying borrowers now have affordable lending options since Fannie Mae and Freddie Mac are operating in loans amounts once only available through jumbo mortgage professionals at higher rates.

With low inventory still an issue, areas with strong wage and job growth could continue to experience home price appreciation in 2022.

So, while purchase-money loans may slow in 2022, the business is certainly not dead.

Increases in home equity will provide lenders with exciting opportunities.

8 Top Mortgage Lead Strategies for 2022

1. Loan Consolidation Leads

Consumers often use second mortgages as a strategy to put less money down when purchasing a home, refinance high-interest-rate debt, or pull money to take care of home repairs. Second mortgages have higher rates than first mortgages. Mortgage professionals could greatly help owners with seconds refinance into a single, long-term loan with a lower rate than their current blended rate on existing mortgages.

The data needed to discover these mortgage leads will be properties where the owners have more than two loans and the combined loan-to-value is less than 80%. See this sample quick list for PMI elimination leads in Florida with an estimated 378,000 loan consolidation leads.

2. PMI Elimination Leads

Private mortgage insurance, or PMI, will be a no-brainer strategy for 2022. Imagine reaching out to any customer that closed a loan with you over the last three years, letting them know you can save them money. Depending on the loan amount, it could easily mean hundreds in savings every month. Even if mortgage rates increase in 2022, getting rid of the PMI means more money in your customers' pocket, which would help offset slight increases in loan amounts. Actively managing past loan clients could also be a boon for the referral business.

The way to discover these PMI mortgage leads is by looking for properties where the current first mortgage has a loan-to-value of more than 80%, and the present combined loan-to-value is now less than 80%. See this sample quick list for PMI elimination leads in Texas where there is an estimated 1.1 million PMI elimination leads.

3. HELOC and Cash Out Prospect Leads

Inventory was so low in 2021, it isn't unusual to hear stories of buyers overpaying for properties due to stiff competition. This sometimes led to owners being unable to do needed or wanted repairs since they had to bring more cash in to close the deal. With equity gains, mortgage professionals can help even recent clients obtain HELOCs, allowing them to do home repairs, pay off high-cost debts, or even pay for college tuition.

The data used to source HELOC leads looks at properties with a combined loan-to-value of less than 70%. See this sample quick list for HELOC loan leads in Idaho, where there are an estimated 453,000 leads.

4. Cash-Out Refinance Leads

Unlike a HELOC, a cash-out refinance locks in today's interest rate for the life of the loan. Depending on how the consumer plans to spend the money, even if mortgage rates increase, the new loan rate may be far superior to what the customer will pay on credit cards, school debts, and other high-cost debts.

The data used to source cash-out refinance opportunities looks for properties with at least 30% equity. See this sample quick list for cash-out refinance loan leads in Missouri, with an estimated 1.2 million loan leads.

5. Renovation Loan Leads

Some consumers choose to upgrade and renovate their current homes instead of going through the hassle of moving. With renovation loans, the property's age is a key criterion to discover renovation loan leads for products like Fannie Mae's HomeStyle Renovation Loans or Freddie Mac's CHOICERenovation Mortgages. Some states are promoting the construction of accessory dwelling units (ADUs) to address housing shortages. Renovation and cash-out refinances are two loan strategies that can help owners get the money they need to construct these secondary units, which can serve as a home office, flex space, space for aging parents, or to produce extra income for the family.

The data used to source renovation loan leads include properties at least 20 years old where the owner has 30% or more equity. You can further drill down to specific periods by looking at the transfer dates. See this sample quick list for renovation loan leads in Tennessee where the owners purchased the property between January of 2014 and December of 2017. There are currently an estimated 160,000 loan leads with these criteria.

6. Reverse Mortgage Leads

10,000 Baby Boomers are retiring every day. Seniors on a fixed income may not be as equipped to handle inflation, and their homes may be a great source of money to help them in their retirement.

The data used to source reverse mortgage opportunities use owners at least 62 years old with an estimated combined loan-to-value of less than 50%. See this sample quick list for reverse mortgage leads in Georgia, with an estimated 717,000 loan leads.

7. Cash-Out Refinance for College Leads

The UC system saw record numbers of college applicants thanks to waived standardized testing requirements during the pandemic. Parents looking to find a less expensive way to finance higher education need to look no further than their home equity.

The data used to source college loan leads looks for an estimated equity position of at least 30% where the owner has children ages 16-17 in the home. See this sample quick list for cash out for college loan leads in California, with an estimated 450,000 loan leads. Other interesting criteria to stack include whether or not the current owners themselves have college degrees making it more likely a college education is a priority for the family.

8. Landlord Bulk Refinance

Investors who purchased rentals starting in 2009 often purchased rental properties far below replacement cost. Loan originators who work with flip investors know that investors can be a great source of leads when flipping and reselling to owner-occupants. However, landlords offer another lucrative opportunity. Landlords with rental portfolios can save thousands monthly by refinancing out of hard money or vintage loans at higher interest rates. While portfolio refinances can take work, the payoff is doing numerous loans at one time.

The data used to source landlord portfolio refinance leads looks for owners with 10+ properties. See this sample quick list for landlord bulk refinance leads, narrowed by looking at properties purchased in Nevada between January 2009 and December 2017. There are 21,000 loan leads in Nevada that meet these criteria.

Connecting with Your Mortgage Leads

Pulling mortgage lead lists using a tool like PropertyRadar that includes enhanced public records data and criteria like demographic data, email addresses, and phone numbers open new ways for lenders and loan originators to connect with current customers and prospects. Not only can messages be tailored to one of the eight strategies listed above, but marketing can also be highly personalized for increased engagement.

Mortgage professionals may want to expand or stack marketing channels in 2022 using the following:

Direct mail. Mailers have long been a staple marketing channel for the mortgage industry. However, as mailing costs continue to rise, there's more pressure to measure ROI. Lists and messaging should be hyper-targeted, localized, and personalized.

In 2022, don't forget that design matters. From the shape and size of the mailer to the branding and colors used to communicate your lending programs, explore new ways to stand out in 2022. When testing new designs or messaging, carefully select one thing to change at a time.

Cold Calling. Federal and state rules dictate what mortgage pros can and cannot do in telemarketing to Established Business Relationships (EBRs). The FCC Telephone Consumer Protection Act and the FTC Telemarketing Sales Rules regulate robocalls and telemarketing at the federal level. Mortgage professionals that illegally call numbers on the National Do Not Call Registry or place an illegal robocall can currently face up to $43,792 in fines per call!

If a contact asked for information within the past three months or they've closed a mortgage loan with your business in the past 18 months, you have an established business relationship that allows you to contact them. If cold calling or text marketing are channels you want to explore in 2022, point your call-to-action to specific channels and get permission to communicate with them legally in those channels.

SMS & VMD. Cold text message and voice mail drop marketing will continue to be a challenge in 2022. It falls under the same guidelines as cold calling. Express permission is required if you want to avoid hefty fines. Even with express permission to text message existing prospects and customers, follow best practices. Make messages sound more human than robotic, make it easy to opt-out, use a real phone number, and keep records of consent.

Text marketing has become wildly popular because of its 98% read rate and low delivery cost compared to other marketing methods. However, one FTC complaint and a five-figure fine could easily wipe out any savings, so proceed with caution and stay on top of regulations around this marketing strategy.

Email Marketing. Email marketing will continue to be a popular outlet in 2022. Permission-based email marketing is not only a best practice but imperative if mortgage professionals want prospects and customers to see their message.

The FTC may not fine you for cold emailing prospects, but email service providers can easily block unwanted emails before they ever arrive in the user's inbox. If messages do get through, unwanted emails will likely land in spam and other folders well known for immediate deletion. Worse, if you use email marketing platforms to send out messages and too many consumers complain, the service provider can completely shut down your entire account! As you're developing marketing funnels, double opt-in permissions are the way to go to stay compliant.

Facebook marketing. Customer matching on Facebook allows you to use email addresses from existing mortgage customers to market directly on Facebook. Look-alike audiences can further extend your reach to prospects that look like your current customers on Facebook. Drive leads to your own marketing channels and get opt-in permissions for marketing channels you control.

Unique Mortgage Lead Opportunities Abound For You In 2022

Purchase mortgages will keep mortgage professionals busy in 2022, but the huge increase in equity gives you new opportunities to keep your pipeline full of quality leads and generate business in 2022 and beyond.

If you are ready to grow your business and want access to the opportunities we just discussed, sign up for your free trial with PropertyRadar today.